Maintaining healthy cash flow is one of the biggest challenges small and mid-sized businesses face today. Whether you’re covering payroll, purchasing inventory, or preparing for seasonal slowdowns, the ability to access working capital quickly can make or break your business. That’s where working capital loans come into play.

In this post, we’ll break down what working capital loans are, how they can benefit your business, and how you can secure the best funding options—plus why Money Man 4 Business is a trusted partner for business owners across the U.S. looking for fast, flexible funding.

What Is a Working Capital Loan?

A working capital loan is a type of short-term financing that helps businesses cover day-to-day operating expenses. These expenses may include:

-

Rent or lease payments

-

Payroll

-

Utilities

-

Inventory and supplies

-

Marketing and advertising

-

Unexpected costs

Unlike long-term loans used to purchase real estate or equipment, working capital financing is designed to fill temporary gaps in cash flow, especially during periods when revenues dip or expenses increase.

Why Cash Flow Management Matters

Cash flow is the lifeblood of your business. A profitable business can still fail if it doesn’t manage cash flow properly. For example, if customers take 60 days to pay invoices, but you need to pay suppliers and staff every two weeks, you could run into a cash crunch.

Working capital loans help bridge this gap—giving you immediate access to the funds you need to keep operations running smoothly.

Types of Working Capital Loans

There’s no one-size-fits-all solution when it comes to financing. Here are the most common types of working capital loans available to business owners:

1. Term Loans

These are traditional loans where you receive a lump sum of capital upfront and repay it over a fixed period with interest. They are ideal for covering one-time expenses like bulk inventory purchases or temporary cash flow issues.

2. Business Line of Credit

A flexible financing option that works like a credit card. You’re approved for a set amount of capital and can draw funds as needed—only paying interest on what you use. Perfect for managing ongoing cash flow fluctuations.

3. Invoice Financing

If you’re waiting on outstanding invoices to be paid, invoice financing allows you to borrow against those receivables—providing cash today while you wait for customer payments.

4. Merchant Cash Advances

This option provides an upfront sum in exchange for a percentage of your future sales. It’s fast and easy to qualify for, but typically carries higher fees.

5. SBA Working Capital Loans

Backed by the U.S. Small Business Administration, SBA loans offer low rates and long repayment terms. Options like the SBA 7(a) Loan and SBA 504 Loan can be used for working capital under certain conditions.

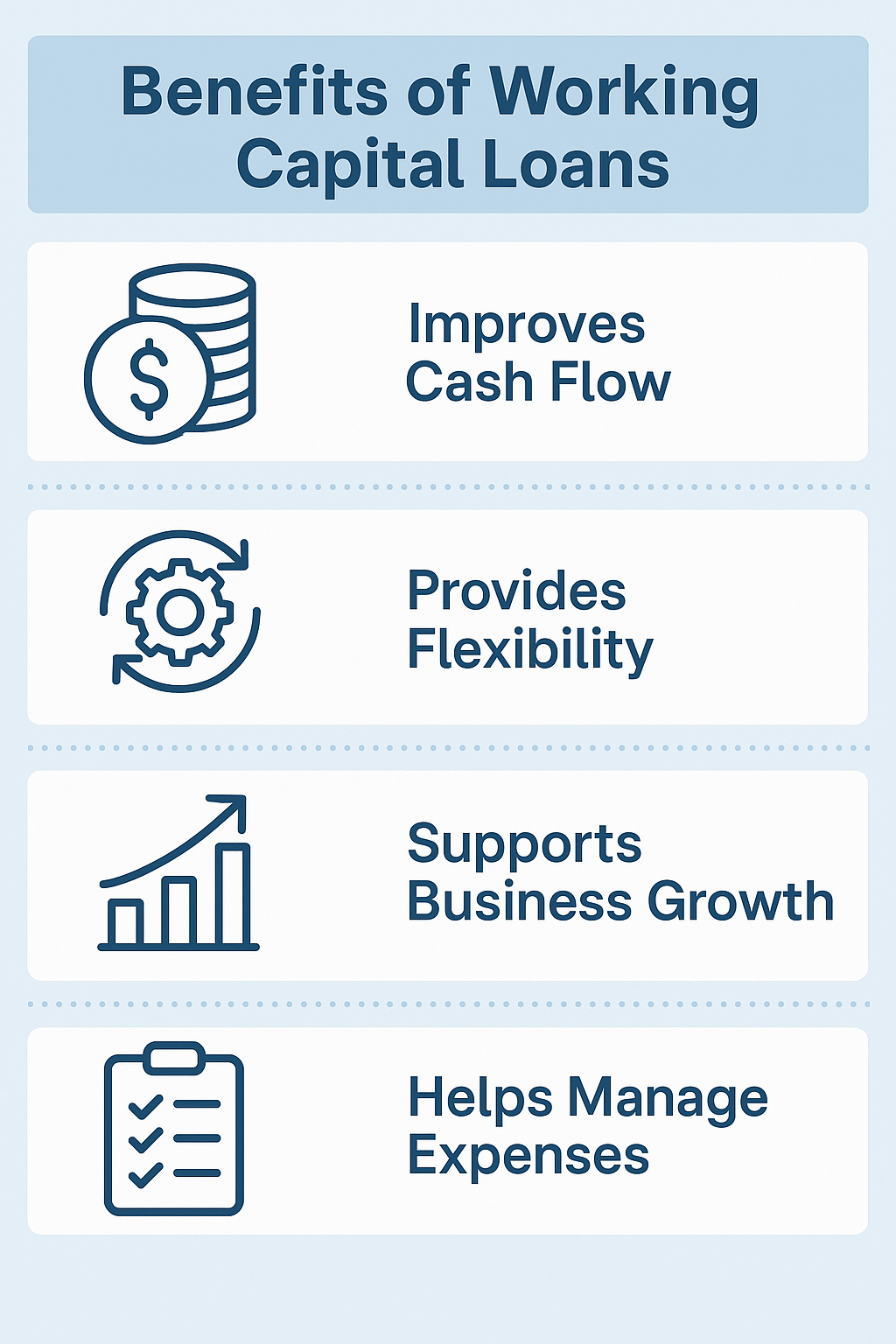

How Working Capital Loans Help Your Business Thrive

Here’s how access to working capital can positively impact your business operations:

✅ Maintain Smooth Operations

Avoid disruptions in your day-to-day operations by ensuring bills, rent, and payroll are always covered—even when cash is tight.

✅ Handle Seasonality with Ease

Many businesses experience fluctuations in revenue throughout the year. Working capital loans allow you to prepare for slower months without stress.

✅ Take Advantage of Growth Opportunities

Want to buy inventory in bulk at a discount? Launch a new marketing campaign? Working capital gives you the flexibility to say “yes” to growth when opportunity knocks.

✅ Avoid Long-Term Debt

Short-term working capital loans offer fast solutions without tying you down with long-term liabilities.

✅ Improve Credit Score

Making timely repayments on your loan can help build your business credit profile, giving you access to larger funding amounts in the future.

Who Can Benefit from a Working Capital Loan?

Working capital loans are ideal for a wide variety of businesses, including:

-

Retail stores and e-commerce businesses

-

Restaurants and hospitality services

-

Professional services firms (consultants, agencies, etc.)

-

Medical and dental practices

-

Construction companies

-

Manufacturing and wholesale businesses

Whether you’re a startup navigating early challenges or an established company seeking to grow, working capital loans offer the flexibility and support you need.

Requirements for Working Capital Loans

While requirements vary by lender and loan type, you’ll typically need:

-

A minimum credit score of 600–650

-

3 to 12 months of bank statements

-

At least 6–12 months in business

-

Proof of revenue (usually $10,000+/month)

-

Personal and/or business tax returns (for larger loans)

Need help figuring out what you qualify for? Money Man 4 Business can walk you through it.

Real-World Examples of Working Capital Loan Offers

Here are just a few recent examples of approved funding options:

-

$635,800 at 10.50% for 5 years — Monthly payment: $14,444.95

-

$450,000 at 10.50% for 10 years — Monthly payment: $6,072.07

-

$100,000 at 11.99% for 3 years — Monthly payment: $3,320.95

Each option is tailored based on your credit profile, revenue, and business needs.

⭐ Why Choose Money Man 4 Business?

At Money Man 4 Business, we specialize in helping entrepreneurs and business owners get the funding they need—with speed, flexibility, and transparency. Here’s what sets us apart:

🔹 Fast Application Process

Apply in minutes with minimal documentation. We respect your time.

🔹 High Approval Rates

We work with a wide network of lenders to match you with the best possible offer—even if you’ve been turned down elsewhere.

🔹 Personalized Support

Our team takes the time to understand your goals and recommend financing options that truly fit your needs.

🔹 Transparent Terms

No hidden fees. No surprises. Just honest business funding.

🔹 Free Credit Score Check

Free Credit score check

Ready to take control of your cash flow? Apply now or schedule a free consultation with one of our funding experts.

💡 Pro Tip: Use a Business Line of Credit as a Safety Net

A business line of credit is one of the best tools for managing unpredictable cash flow. It gives you access to funds whenever you need them—without needing to reapply. Many savvy business owners keep a line of credit open just in case.

Money Man 4 Business offers Business Lines of Credit up to $500,000 at rates as low as 6.00%, available with any term loan of $250,000 or more.

📈 Boost Your Business Today with Flexible Funding

Working capital loans are more than just a quick fix—they’re a powerful tool for business stability and growth. Whether you need $25,000 to bridge a short-term gap or $500,000 to fuel expansion, Money Man 4 Business is here to help.

Let us help you get the capital you need, when you need it—without the hassle.

✅ Get Started Today

Your next business breakthrough might be just one loan away.

👉 Apply Now

👉 Or call us for a free consultation: (888.882.2741)

Money Man 4 Business—Your trusted partner for business loans, working capital financing, and cash flow solutionsthat work.

Also Check our State Wise Business Loan Data.

Understanding Small Business Loans

Understanding Small Business Loans