In the ever-evolving world of small business financing, finding the best business loan providers 2025 can be a game-changer for entrepreneurs seeking to grow, stabilize, or scale their operations. With countless lenders flooding the market, making the right choice is overwhelming. But what if you had a trusted partner that simplifies the process, offers transparent terms, and understands your unique business needs?

Enter Money Man 4 Business – your dedicated small business loan specialist.

In this detailed comparison, we’ll explore how Money Man 4 Business stands out from “other” lenders in 2025, and why it should be your first choice for business financing.

Why Choosing the Right Business Loan Provider Matters in 2025

Small businesses are the backbone of the economy. Whether you’re expanding, managing cash flow, or investing in new opportunities, the right loan can fuel your success. However, hidden fees, rigid qualification criteria, and slow approvals often frustrate business owners.

That’s why it’s crucial to partner with a lender who:

✅ Understands your business challenges

✅ Offers flexible loan solutions

✅ Provides quick and transparent approvals

✅ Supports you beyond funding

This is exactly where Money Man 4 Business makes a difference.

Types of Business Loans Offered by Money Man 4 Business – best business loan providers 2025

Before comparing, let’s understand the variety of business loan solutions available through Money Man 4 Business:

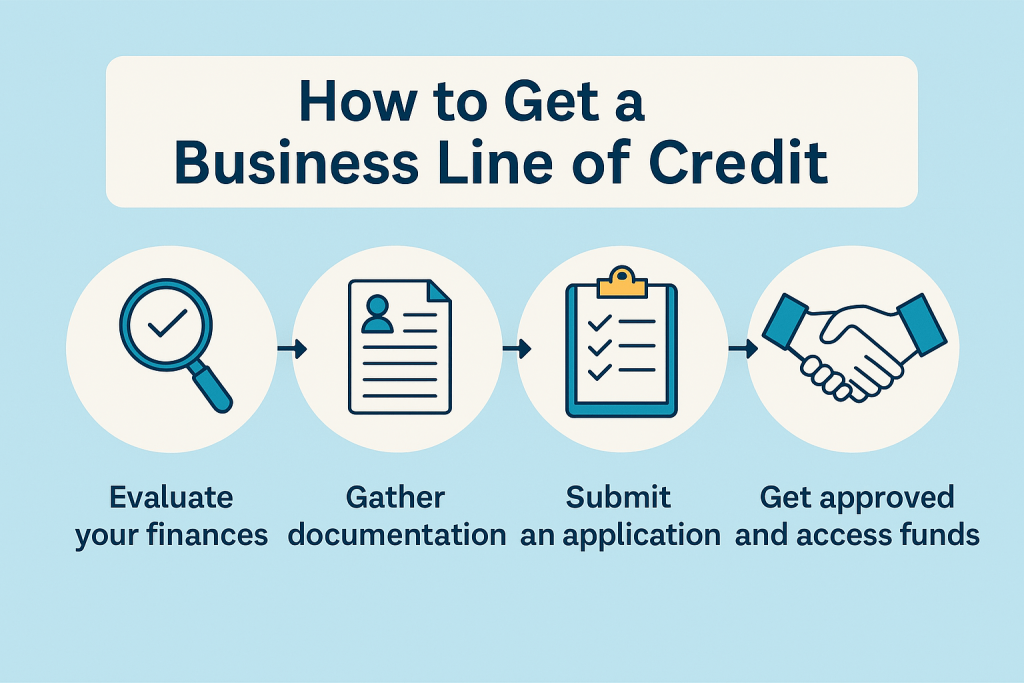

1. Business Line of Credit

A flexible funding option allowing businesses to draw funds as needed and pay interest only on the used amount. Ideal for managing cash flow, inventory purchases, or unexpected expenses.

2. Term Loans (1-25 Years)

Fixed-term business loans with predictable repayment schedules. Perfect for major investments like equipment, expansion, or large working capital needs.

3. SBA Loans (7a & 504)

Government-backed small business loans with competitive rates and extended terms. Money Man 4 Business simplifies the complex SBA loan application process for faster approvals.

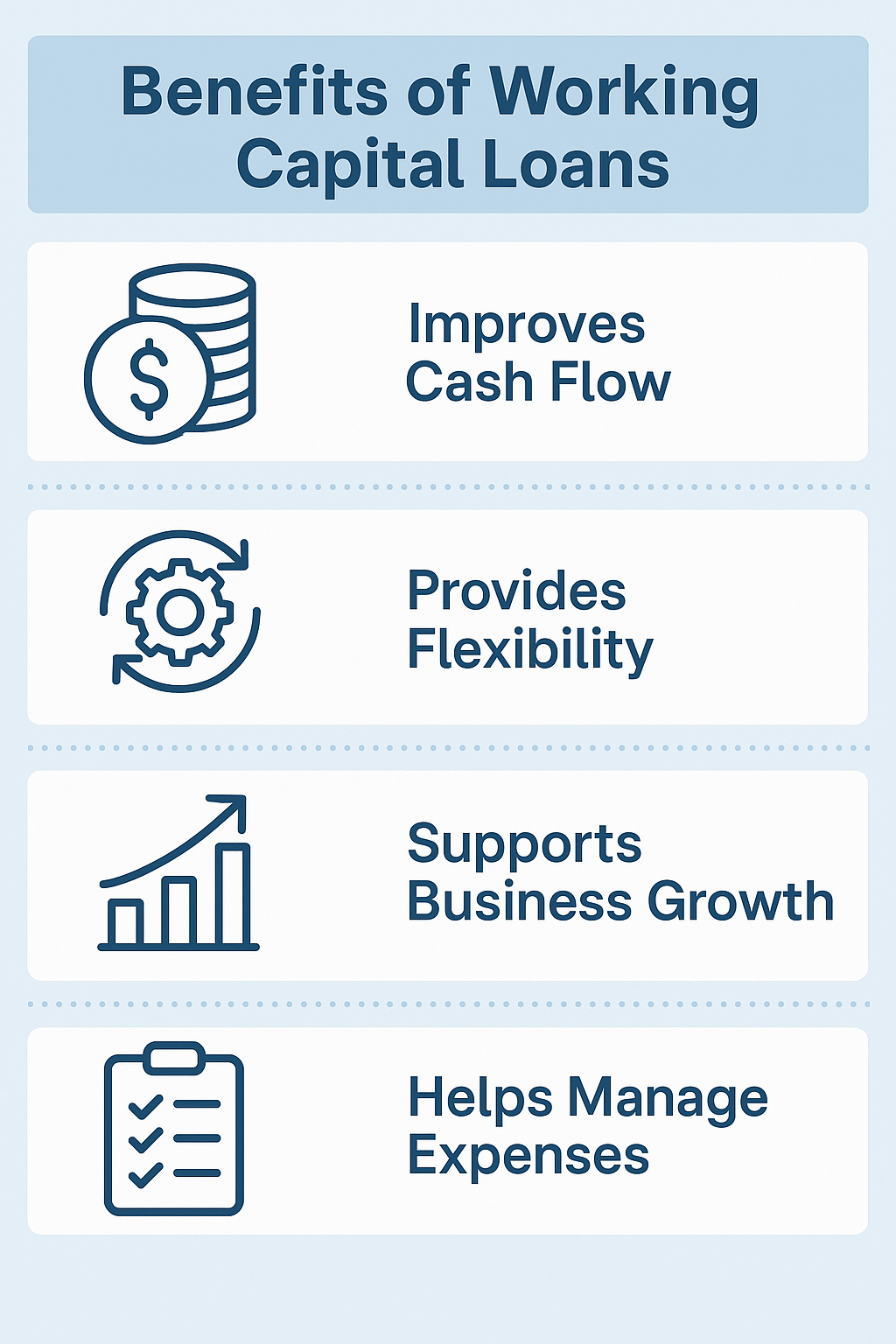

4. Working Capital Loans

Short-term financing to manage daily operational costs, payroll, rent, and seasonal cash flow gaps.

5. Business Equipment Financing

Tailored loans to purchase machinery, vehicles, or technology essential for your business operations.

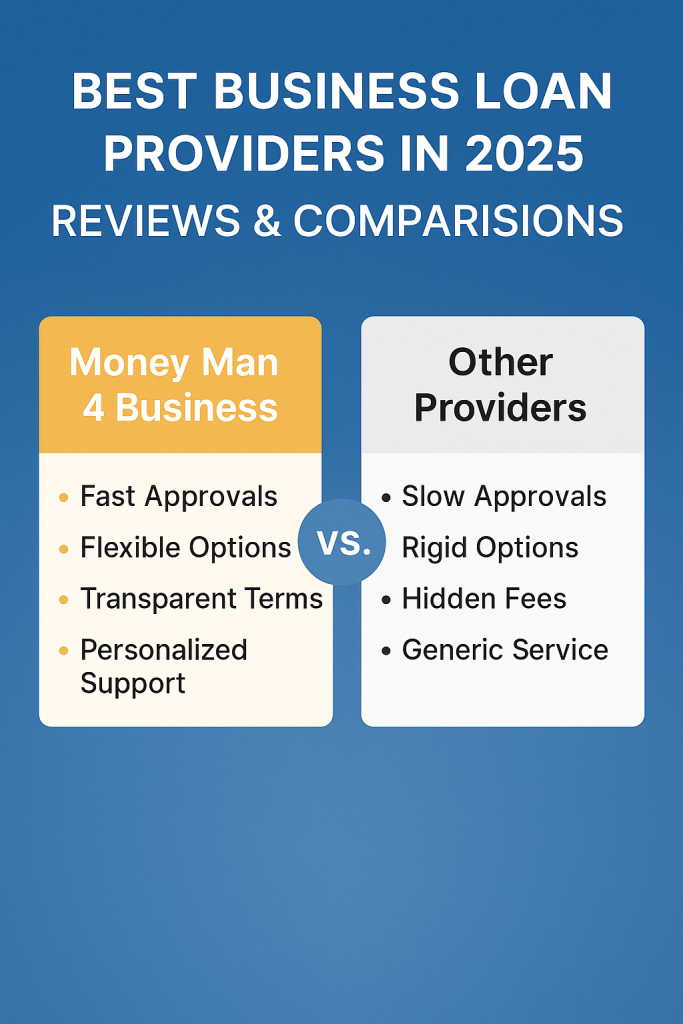

Money Man 4 Business vs. Other Loan Providers: The Key Differences

Let’s dive into the factors that differentiate Money Man 4 Business from typical lenders:

| Feature | Money Man 4 Business | Other Lenders |

|---|---|---|

| Approval Speed | 24-48 hours for pre-approval | Can take weeks |

| Documentation | Simplified, minimal paperwork | Lengthy, complex requirements |

| Loan Flexibility | Custom-tailored solutions | Rigid, standard loan packages |

| Interest Rates | Competitive with transparent terms | Hidden fees & variable rates |

| Qualification Criteria | Supports businesses with low credit | Strict credit score benchmarks |

| Personalized Support | Dedicated loan advisors | Generic customer service |

| Funding Amounts | From $10,000 up to $5 Million | Often limited to smaller amounts |

| Reputation | Focused on small business success | Profit-driven, less personalized |

| Technology Integration | Easy online application & tracking | Outdated processes |

Customer Reviews: Why Businesses Prefer Money Man 4 Business

Here’s what satisfied business owners are saying about their experience with Money Man 4 Business:

⭐️⭐️⭐️⭐️⭐️

“Money Man 4 Business made the loan process hassle-free. I got approved in 2 days, and the funds were in my account within a week. Their team understood my business needs and offered the best possible solution.”

— Ravi S., Restaurant Owner

⭐️⭐️⭐️⭐️⭐️

“Unlike other lenders, Money Man 4 Business didn’t judge me for my low credit score. They looked at my business potential and helped me secure a working capital loan that saved my operations.”

— Priya M., Retail Shop Owner

⭐️⭐️⭐️⭐️⭐️

“Transparent, quick, and supportive — that’s how I’d describe Money Man 4 Business. Highly recommended for small business owners who need reliable financing.”

— John P., Logistics Business Owner

Common Problems with “Other” Business Loan Providers

Choosing the wrong lender can cost you more than just money. Here are typical challenges businesses face with other loan providers:

❌ Hidden Fees & Complex Terms

Many lenders offer seemingly attractive rates but bury fees in the fine print.

❌ Slow Approval Process

Time-sensitive funding needs get delayed due to excessive documentation and slow processing.

❌ Rigid Eligibility Requirements

High credit score demands and revenue thresholds disqualify many small businesses.

❌ Lack of Personalized Support

Businesses are treated as numbers, not valued partners, resulting in poor customer experience.

With Money Man 4 Business, these issues are effectively eliminated.

Why Money Man 4 Business is the Best Choice in 2025

Here’s a quick summary of why Money Man 4 Business is the best business loan provider in 2025:

✅ Fast & hassle-free approvals

✅ Customized loan solutions for every business

✅ Transparent terms with no hidden fees

✅ Flexible qualification criteria

✅ Dedicated loan advisors for personalized support

✅ Competitive interest rates

✅ Proven track record of supporting small businesses

When you choose Money Man 4 Business, you’re not just getting a loan — you’re gaining a reliable financial partner committed to your success.

How to Apply for a Business Loan with Money Man 4 Business

The application process is designed for busy business owners. Here’s how it works:

-

Online Application

Fill out a simple form on the Money Man 4 Business website with your business details. -

Pre-Approval in 24-48 Hours

Receive a pre-approval decision quickly, so you can plan accordingly. -

Personalized Consultation

A dedicated advisor will contact you to understand your needs and recommend the best loan option. -

Final Approval & Funding

Submit minimal documentation and receive funds in your account in as little as 5-7 business days. -

Ongoing Support

Even after funding, Money Man 4 Business stays connected to support your business growth.

Conclusion: Make the Smart Choice for Your Business

In 2025, small business success depends on agility, access to capital, and reliable partners. Money Man 4 Business is your go-to solution for all business financing needs, offering unmatched flexibility, speed, and personalized service compared to other loan providers.

Don’t let rigid banks and hidden fees hold you back.

Partner with Money Man 4 Business and empower your business growth today.

➡️ Apply Now at Money Man 4 Business and get the funding you deserve.

Understanding Small Business Loans

Understanding Small Business Loans