(Money Man 4 Business Do Not Charge Any Fee For The Application.)

Sorry. PPP 2 Application form is no longer available as the Paycheck Protection Program (PPP) ended on May 31, 2021. Existing borrowers may be eligible for PPP loan forgiveness.

President Biden has made changes to the PPP loan program.

Notes:

A common challenge many self-employed individuals face is that they may not have yet to file their 2020 taxes. You can provide your lender a draft of your 2020 Schedule C that you will file with the IRS.

New Paycheck Protection Program (PPP) rules that allow eligible self-employed individuals who file Form 1040, Schedule C, to calculate their maximum loan amount using gross income instead of net profit. This may increase the amount of funding most eligible self-employed individuals can qualify for.

Only Five Steps if you want to use 2020 information for your PPP loan application prior to filing your 2020 taxes. March 31, 2021 PPP2 ends for new applications.

- Now New Changes. More funding for PPP2, You may qualify for PPP2 for more funding.

- No longer using Line 31, Use Line 7, Gross Income, Schedule C

- Use Gross Income, divide in to 12 months, multiply by 2.5 = Your Benefit.

- Self-Employed, Independent Contractors, and Gig Economy Workers can Apply for PPP Loan Prior to filing 2020 Taxes.

There was a problem with your submission. Please review the fields below.

The Paycheck Protection Program remains open for First and Second Draw PPP loans until March 31, 2021, as set forth in the Economic Aid Act, or until Congressionally appropriated funding is exhausted. The maximum amount of a Second Draw PPP loan is $2 million.

Eligible Entities Have a Second Chance to Receive a PPP Loan

There are many businesses who were not able to receive the first round of PPP loan and many businesses also requested for a 2nd round of PPP loan. So, the new proposed bill allows new and old business to receive 2nd round of PPP loan only if they meet the required eligibility.

Eligible Entity: Schedule C or F, income and expenses from a sole proprietorship, or bank records (not a schedule F farmer or Schedule E landlord), An LLC or other entity treated as a partnership or an S Corporation that meets following requirements:

- Businesses at least have a 25% reduction in gross receipts in a quarter in 2020 compared to same quarter 2019. The gross receipt will include all revenues of the business including expenses from the business normal operation for the purpose of this 25% rule.

- Business must have less than 300 employees or meet an alternative size standard.

Were you not in Business in 1st, 2nd or 3rd quarter of 2019?

If a business was not in operation during the 1st, 2nd or 3rd quarter of 2019 which is from 1st January 2019 – 30th September 2019 but were in operation during 4th quarter of 2019 which is between 1st Oct 2019 – 31st Dec 2019, they can compare the 1st, 2nd or 3rd quarter gross receipt of 2020 which is between 1st Jan 2020 – 30th Sep 2020 with the 4th quarter of 2019 gross receipt to calculate the 25% reduction in gross receipt.

Not in Business in 2019 but were in Business by February 15th, 2020?

If a business was not in operation during whole 2019 but was in operation by February 15th, 2020, then such businesses can compare their gross receipt of 1st quarter of 2020 (January 1st, 2020 – March 30th, 2020) with 2nd or 3rd quarter of 2020 (April 1st, 2020 – June 30th, 2020) to see the gross receipt reduction.

Are you a seasonal business? or a New Entity? Or a business with multiple physical location?

Seasonal Business:

If you are a seasonal business, then the maximum amount of PPP round 2 loan is explained below:

The Loan amount will be calculated based on the average monthly payroll cost for a 12 week period selected by the loan applicant. The date must begin from February 15th, 2019 or March 1st, 2019 and ends on June 30th, 2019. If the above dates do not fit for you then alternatively the business may elect any consecutive 12 weeks (any 96 consecutive days) period starting from February 15th, 2020 and ending before January 1st, 2021 multiplied by 2.5. But the loan amount cannot exceed more than $2 million.

New Businesses:

For new businesses, the loan amount can be calculated based upon average monthly payroll costs up through the date the business applies multiplied by 2.5. Again, loan amount cannot exceed $2 million.

Multiple Physical Location Businesses:

For businesses with multiple physical locations, the maximum loan amount for 2nd round of PPP loans is stated as follows:

Maximum $2 million can be the total amount of all covered loans and the Administrator shall not substitute ‘not more than 300 employees per physical location’ for the term ‘not more than 500 employees per physical location’ in paragraph (36)(D)(iii).

Businesses owned 20% or more by Chinese entities are not eligible to receive the 2nd round of PPP loan.

Publicly traded businesses and entities affiliated with the People’s Republic of China are on the list of entities that cannot qualify for a new PPP loan.

PPP Loans Which are Forgiven Will Be Deductible

The IRS has issued a series of Revenue Procedures and Notices that alarmed many PPP borrowers by stating that expenses paid for with forgiven loans will not be able to be deducted. This was against Congress’s intent, and the proposed bill clarifies their position.

PPP Forgiveness Eligibility: Apply here

- 60% of the PPP loan amount must be used for Payroll costs.

- Existing Business mortgage Interest amount can be eligible for forgiveness.

- Business Rents and Utility bill payments also eligible.

- Operations expenditures including office support functions, software and computing costs and processing fees of payrolls.

- Supplier cost which are especially required for business operations.

- Covid-19 safety precaution equipment’s for employees.

- Property damages, vandalism or looting due to public disturbances which are especially not covered under any insurance or compensation.

What is SBA PPP2 (Paycheck Protection Program) loan or PPP round 2 loan?

On December 21st, 2020, Congress passes a long waited Covid-19 relief bill and government funding bill which includes $284 billion for a second round of Pay-check Protection Program (PPP) loan.

Key points:

- Interest rates of 1%

- Maximum Loan Amount $2 Million

- Eligible for Forgiveness or Free money -> Apply here

- No Collateral or Personal guarantees required.

- Business Expenses paid with PPP loans are tax deductible according to CARES Act.

- Business have taken the first round of PPP loan can also apply for second round if eligible.

- 8 weeks to 24 weeks loan forgiveness covered period. 10 months after you can file for forgiveness.

Businesses Eligibility for PPP round 2:

Entity Type: All businesses including nonprofit, veterans’ organizations, tribal concern, self-employed individuals, sole proprietorships, and independent contractors are eligible for forgiveness under below conditions:

- Business must be in operation on February 15th, 2020.

- Small size businesses with 300 or fewer employees.

- First Draw PPP loans- for those borrowers who have not received a PPP loan before August 8, 2020. Are not required to demonstrate a 25% reduction in gross receipts.

OR

- Second Draw PPP loans- for eligible small businesses with 300 employees or less and that previously received a First Draw PPP loan. These borrowers will have to use or had used the full amount of their First Draw loan only for authorized uses and demonstrate at least a 25% reduction in gross receipts between comparable quarters in 2019 and 2020.

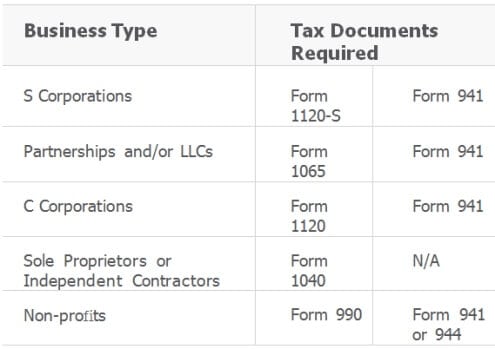

Documents Required:

CARES Act Report

This report is generated straight from your payroll provider like Gusto, Sure payroll, Paychecx, ADP etc. By using this report, the loan processing can be quicker. So, contact your payroll provider and ask for a Cares Act PPP2 Report.

Tax Documents for 2019

Voided Check

You will need to submit a photocopy of voided check front and back from your business bank checking account.

Driver’s License or Passport

You will need to submit a photocopy or scanned copy of your Driver’s license or Passport front and back.

How to apply for SBA PPP Loan?

To Apply for PPP loans, you must follow the process with complex rules and calculations. Any small size Error on PPP application or with documents will leave your application on the table.

If you or your Business has received first round of SBA PPP loans and wants to apply for the second round. We are here to help with all the paperwork for the PPP to get an error free Application. So, what are you waiting for? Use our 29+ years of expertise to do the PPP loan application for you while you run your business smoothly without any worry.

Just call us at: 888.882.2741

Or

Frequently Asked Questions:

Will I eligible for 2nd round of PPP loan if I have already taken in 1st round?

The Answer is YES; you may qualify for 2nd round of PPP loan even after taken the first round of PPP loan and used it completely. Although there are few new eligibility criteria your business needs to meet for the second round of PPP loan. Check eligibility in above article.

Is there any guarantee that I will receive 2nd round of PPP loan after applying?

There is no guarantee of approval of PPP loan as it is completely depending upon SBA eligibility criteria. But you will surely receive a brief explanation of hold or rejection of application within certain time.

I have applied for 1st round of PPP using my bank or using any other lender so can I still apply for the 2nd round of PPP loan with the help of Money Man 4 Business?

Yes, it does not matter if you have applied with another lender, we can still help you with the round 2 PPP application.

Why PPP loans are also called as a Grant? Because this loan amount can be a Free money for you if you follow the Forgiveness Eligibility criteria mentioned above on this article. Yes, that means you do not need to pay the money back just like any grant.

How would I apply for PPP Forgiveness?

Just like PPP application, Money Man 4 Business can also help you with the paperwork for PPP Loan Forgiveness application with a one-time upfront charge of $499. You can inquire for PPP Forgiveness program by visiting PPP Loan Forgiveness and fill the inquiry form.We will call you back and explain the rest of the procedure.

Related Programs

Just call us at: 888.882.2741 Ext 0

Or

Make an Inquiry right now.

")